In January of this year I assessed the market situation and came to the conclusion that the market had eventually bottomed. I have re-assessed the actual situation to try to understand in what direction the market is headed.

I have reviewed following indicators:

- Inflation

- Interest rates

- Purchasing Managers Index (PMI)

- Fiscal Policy

- Treasury Yields

- Curve inversion

- Corporate profits

- Mortgage rates

- New house prices

- New house starts

- Consumer sentiment

- Credit card debt

- US household debt

- Unemployment rate

- Stock Markets

- Market Breadth

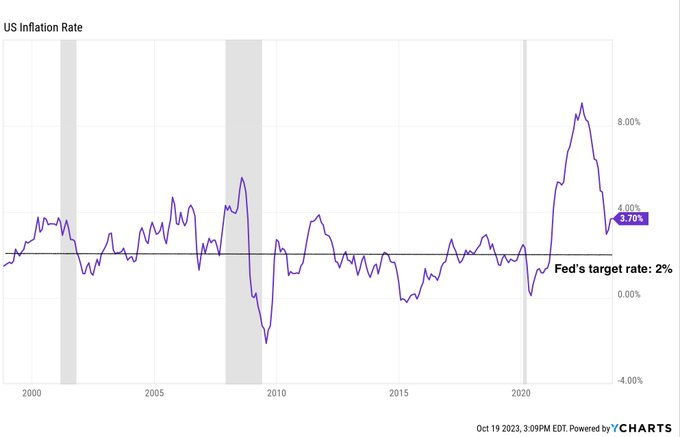

1. INFLATION

Inflation is having difficulties to keep falling, it has even increased in the last three months consecutively from its bottom of 2.97% to 3.70%. Increasing inflation is bad for the economy and the stock market because it forces the Fed to continue increasing rates.

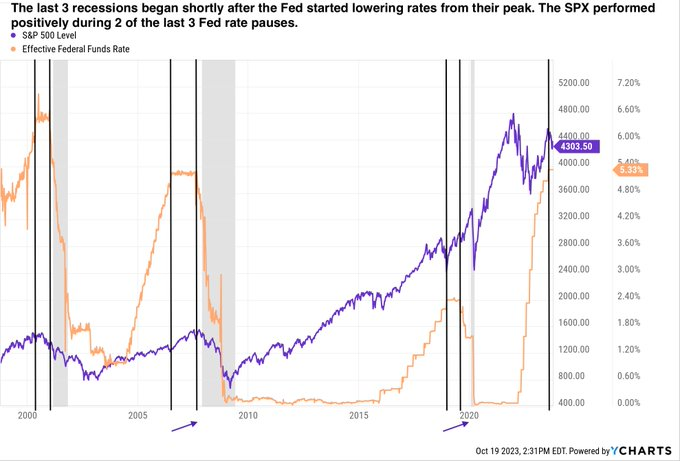

2. INTEREST RATES

Interest rates in the US have reached their 2007 peak. At this point the Fed is expecting something to break. This would be bad news for the economy and the stock market because there could be a big correction and the economy would enter into a recession.

Beginnings of 2023 the market was expecting interest rates to start decreasing in the second half. Now, the market expects rates to decline in the second half of 2024. Lower rates are favorable for the stock market and the economy.

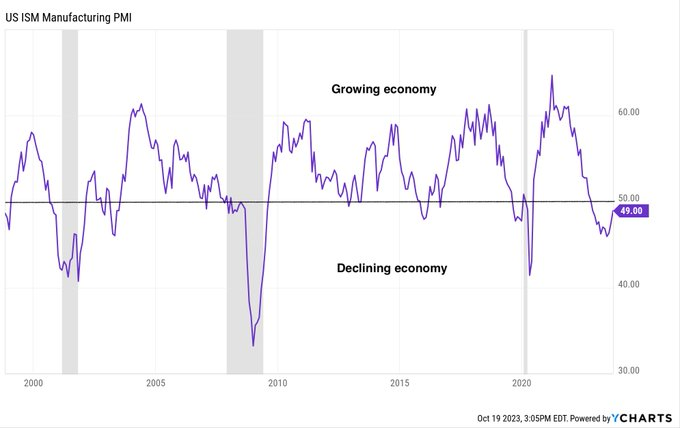

3. PURCHASING MANAGERS INDEX (PMI)

The PMI has been falling since February 2021 to actual 49. When this index is above 50, the economy is considered to be expanding. If it is below, the opposite applies. In June it touched a bottom of 46 but since then it has increased to 49.

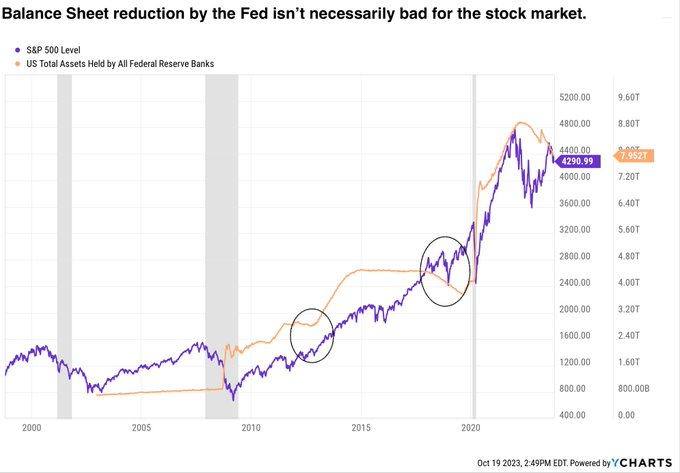

4. FISCAL POLICY

Quantitative tightening by the Fed continues, meaning that it has increased interest rates by hitting a 16 year high of 5-5.25% and it’s reducing its balance sheet (-7% so far this year). The latter doesn’t mean however that the stock market will correct.

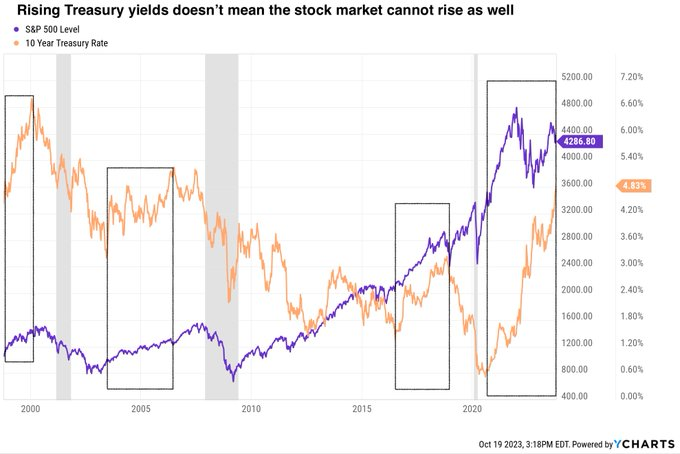

5. TREASURY YIELDS

Yields are the highest in the last 20 years, even higher than in 2007. A zero risk Treasury Note pays almost 5.50% p.a. Having said that, it doesn’t mean the stock market cannot continue to rise despite high treasury yields.

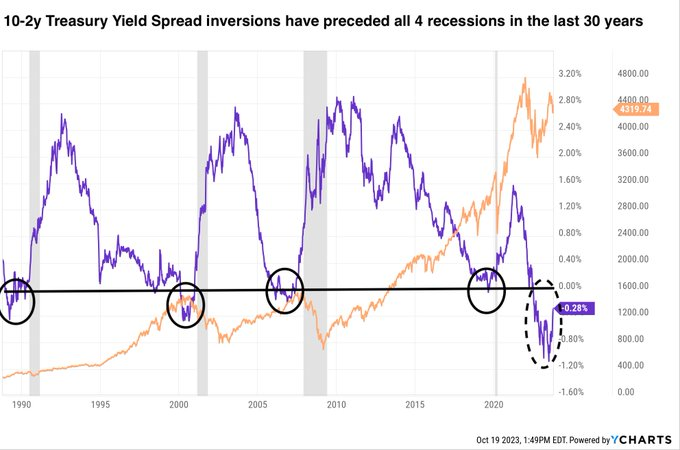

6. CURVE INVERSION

10-2y treasury yield spread inversions have preceded all four recessions we have had since 1990. The S&P has corrected every time. This time it won’t be different. This is bad news for the stock market.

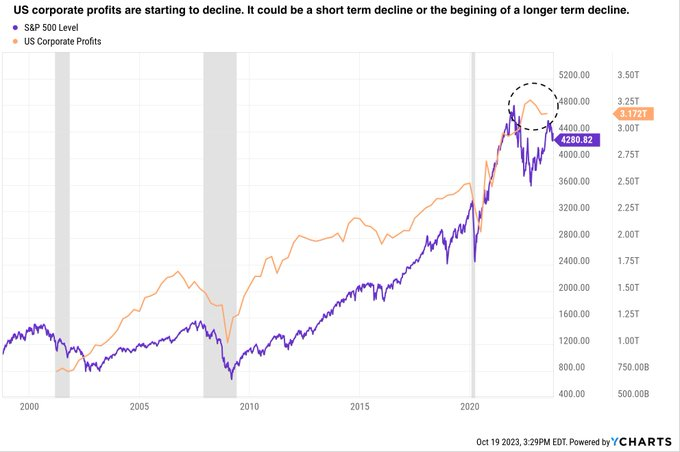

7. CORPORATE PROFITS

US corporate profits came down this year but they have picked up slightly in Q2. We need to wait for the next corporate earning season to see in what direction it develops.

8. MORTGAGE RATES

Mortgage rates are at a 20 year high, however 99% of loans have been locked in a lower rates. Only new applications will be affected. This won’t lower real estate prices quick enough in the short term.

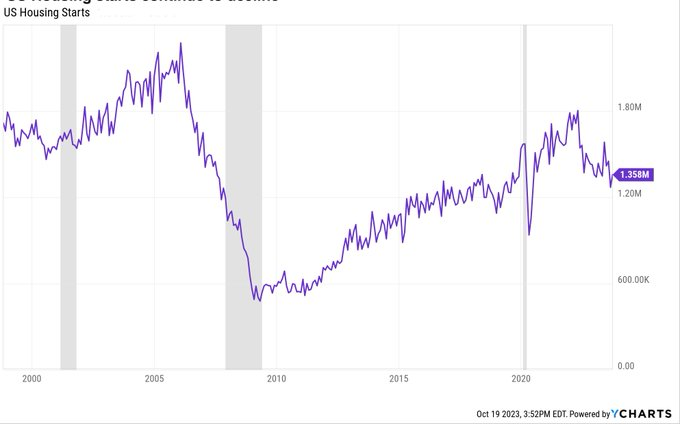

9. US HOUSING STARTS

The high mortgage rates are hurting obviously the new constructions which have fallen 5% in the last 12 months, however there has been a pickup since August.

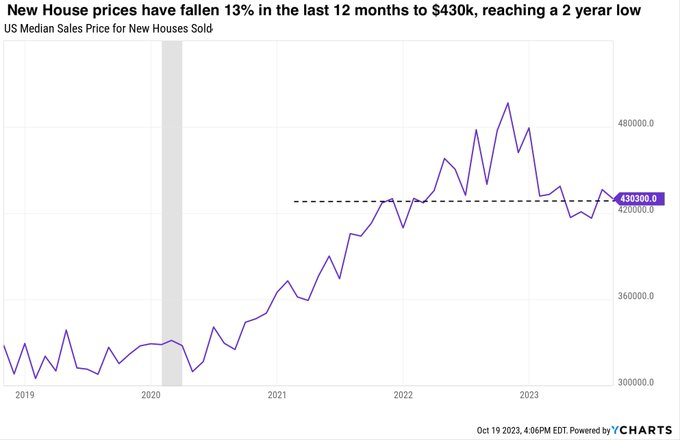

10. US SALES PRICES FOR NEW HOMES

Prices of new homes have fallen 13% in the last 12 months to an avg of $430k. However, inflation is led now by energy prices and not any more by real estate prices, therefore the focus has shifted to the energy market.

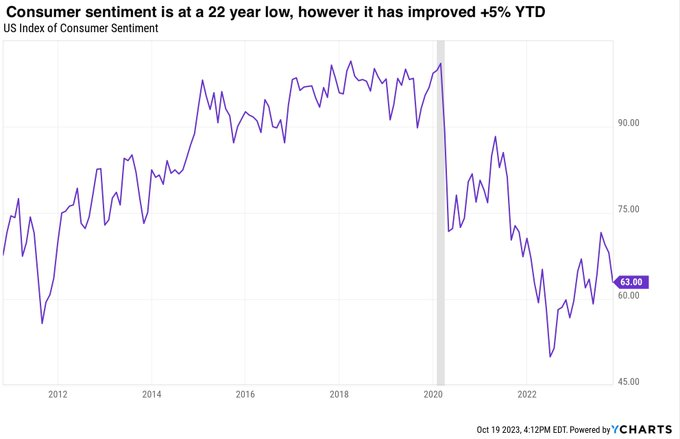

11. CONSUMER SENTIMENT

Is at a 22 year low, even though it has recovered 5% this year.

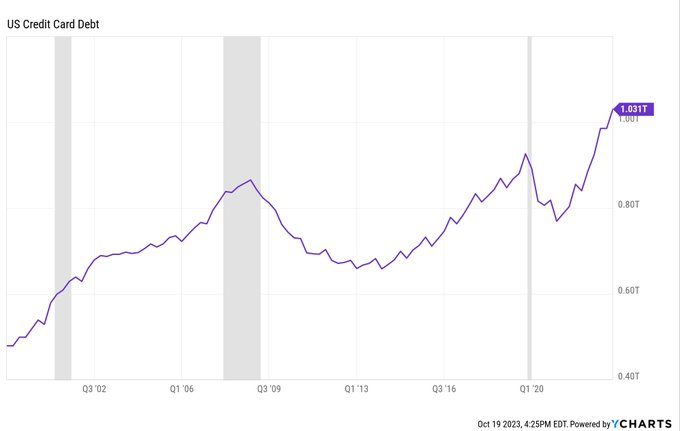

12. US CREDIT CARD DEBT

Credit card debt is at its highest level in the history with interest rates close to 25%. This will hurt the US consumer in the short term, it’s only a matter of time until the consumers slow down their spending.

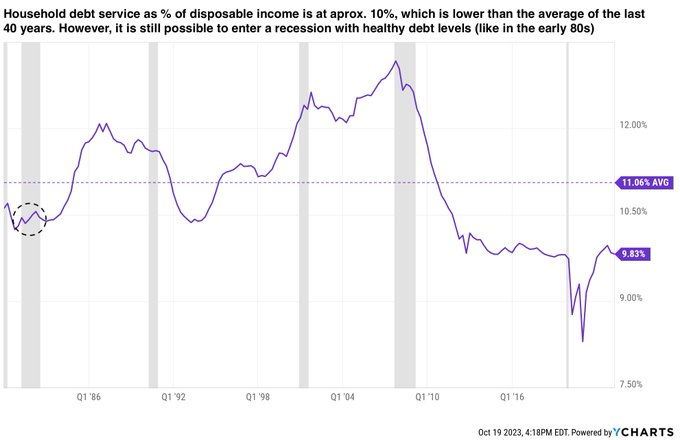

13. US HOUSEHOLD DEBT

The US consumer has still (and amazingly) a healthy financial situation despite of the high credit card debt levels, high interest rates and the high mortgage rates. But it should continue deteriorating.

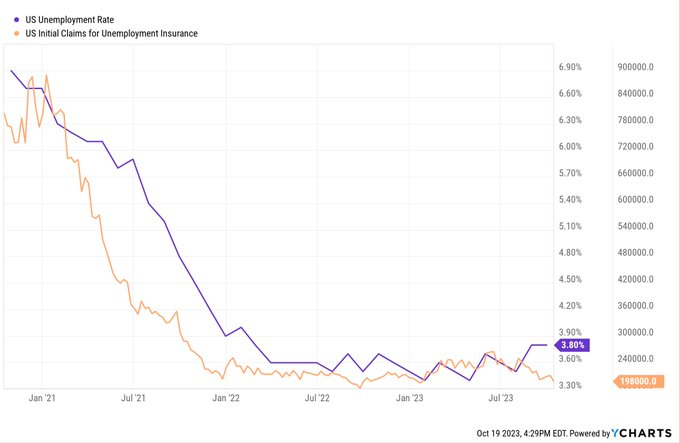

14. UNEMPLOYMENT RATE

The consumer financial health is holding up very well because everybody has a job. The unemployment rate is still very low at 3.80%. Also initial claims for unemployment insurance are at their lowest levels.

15. STOCK MARKETS

The US and European stock market have rebounded from their Oct 22 low and have entered a bull market. However, the market has become very pessimistic due to the wars and the sticky inflation. The SPX is trading below its 50d SMA and almost at the 200d SMA.

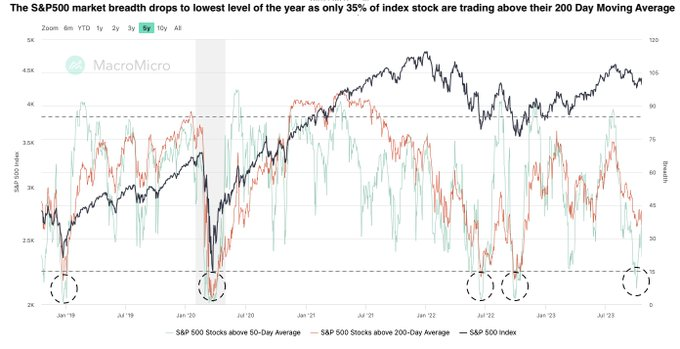

16. MARKET BREADTH

The S&P500 market breadth drops to lowest level of the year as only 35% of index stock are trading above their 200 Day Moving Average. Market breadth hasn’t really been useful to predict market movements but what it does tell us is the following:

1) once it touches bottom the recovery is pretty fast (couple of days),

2) the 50 SMA usually corrects much more than the 200 SMA and it has been below 15% 17 times in the last 17 years, last time being the 4. October 23.

3) every bottom of the 50d SMA matches a bottom in the SPX

4) usually the market takes 11 months on avg to see the next bottom of the 50d SMA breadth but on 9 of 17 occasions the 50d SMA breadth contracted below the 15% level more than once within a few days.

This translates into the actual situation as follows: 1) if there is another bottom we will see it in the next few days. If during the next two weeks we don’t see a new bottom the markets should continue rising for the next few months until the next correction.

CONCLUSION

During the rally of this year we forgot that the Fed has raised interest rates to a record high and has tighten the economy to a point that it’s only waiting for something big to break (the default of some regional banks wasn’t enough) before lowering interest rates. The tightening conditions (high interest rates, record high credit card debt with record high rates, record high mortgage rates) will end up hitting the US consumer.

We have seen in past similar market situations that the markets usually rise during the Fed’s rate pause and that the recession usually hits after the Fed starts lowering interest rates and usually a recession comes along with a market correction.

The curve inversion is for me the most important indicator at the moment because yield inversions have been a reliable predictor of recessions and stock market corrections.

Now that the inversion is headed to normalization (no more inversion) it looks like a recession could come in 2024 along with a the stock market correction. This is the reason why I’m turning cautious for 2024.