Let’s analyze the following pieces of this puzzle:

1. Inflation

2. Central banks

3. Corporate profits

4. Real estate

5. Consumer

6. Stock market

7. Conclusion

1. INFLATION

Inflation peaked in June (9.06%). Now it is at 6.45% (December 22) with a downward trend. We have probably seen the peak and according to the Fed, everything indicates that inflation is going to continue to decline.

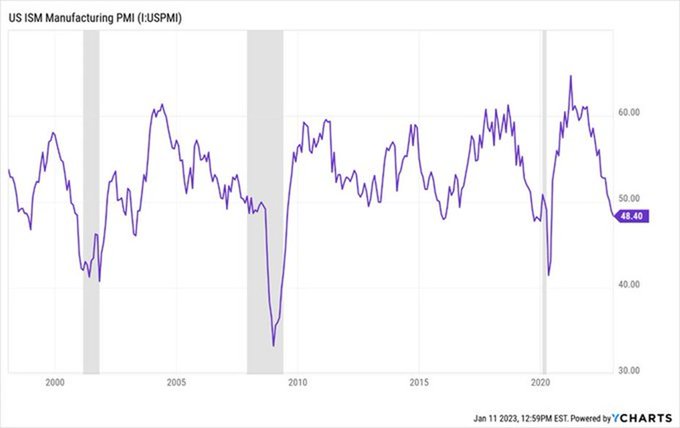

The Purchasing Managers Index (PMI) has dropped from 52.80 in July to 48.40 in December, indicating that the economy is cooling off. When this index is above 50, the economy is considered to be expanding. If it is below, the opposite applies.

2. CENTRAL BANKS

Usually, corporate profits guide the direction of the market. But for a few years the central banks took the reins and became the director of the economic orchestra.

Until 2021, most central banks were in “Quantitative Easing” mode, meaning that they injected liquidity into the economy and kept ultra-low rates to encourage growth. Things changed in 2022 when prices got out of control.

Now, most central banks are in “Quantitative Tightening” mode, meaning that they are raising interest rates and withdrawing liquidity from the market. Let’s see what the major central banks are doing.

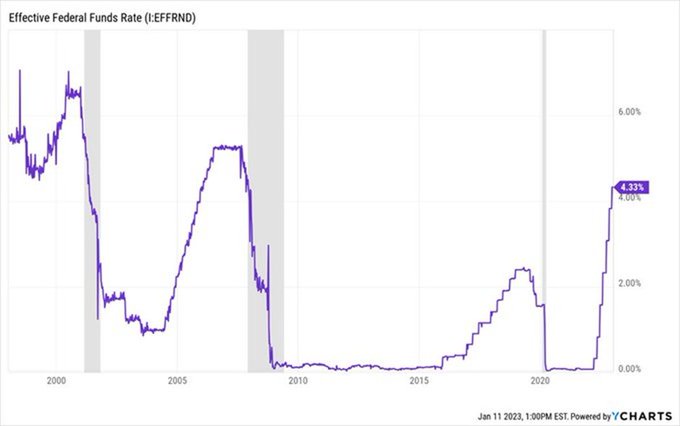

THE FED: The market expects the Fed to raise rates by 25-50bps in February and 25-50bps in March until reaching min. 4.75-5.00% to then pause and eventually start lowering rates again in the second half.

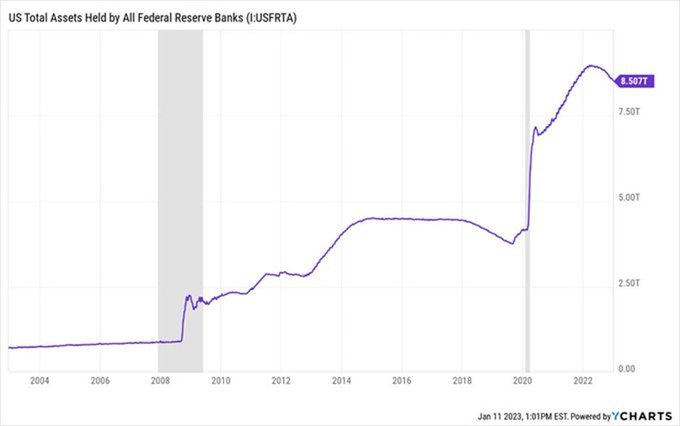

The Fed reduced its balance sheet from $8.76T to $8.555T in 2022, which corresponds to a reduction of $206B. This reduction is part of the “Quantitative Tightening”. With this measure, the Fed reduces market liquidity and sells assets.

The Fed indicated that it would reduce its balance sheet from mid-2022 by $47.5B per month and from Sept by $95B per month, but in reality, it has been reducing it much less. In December it reduced it by only $34B. The Fed is managing its balance sheet very cautiously.

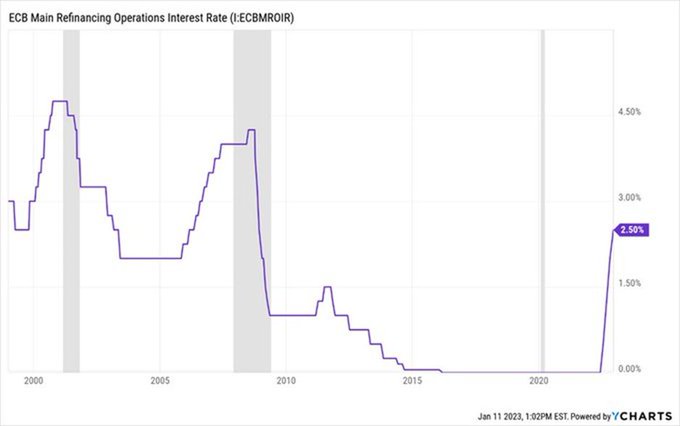

The European Central Bank (ECB) increased after 6 years (!) interest rates from 0% to 2.50% in 2022 and is still in the bullish cycle.

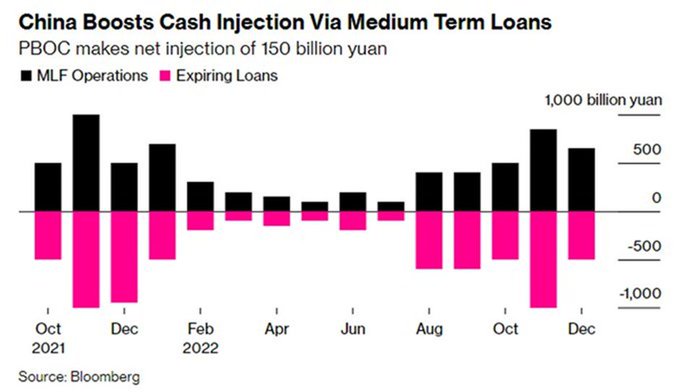

The Chinese central bank (PBOC) is taking another direction compared to the US and the EU. They are injecting liquidity into the economy – which is known as “Quantitative Easing”. In December 2022 the PBOC injected $94B, $20B more than expected by analysts.

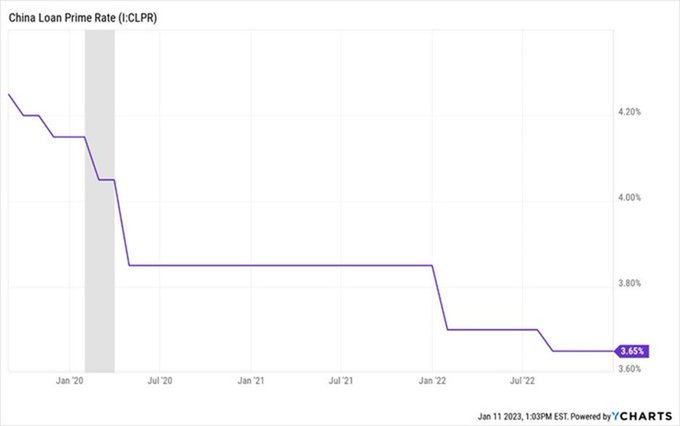

The PBOC cut interest rates in 2022 from 3.85% to 3.65% and continues in its downward cycle. In other words, China is ahead of the economic cycle compared to the rest of the major central banks. China can afford this because it has inflation under control (1.60%).

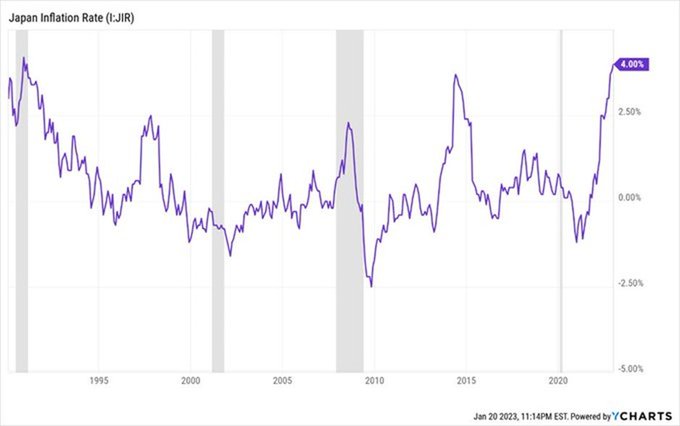

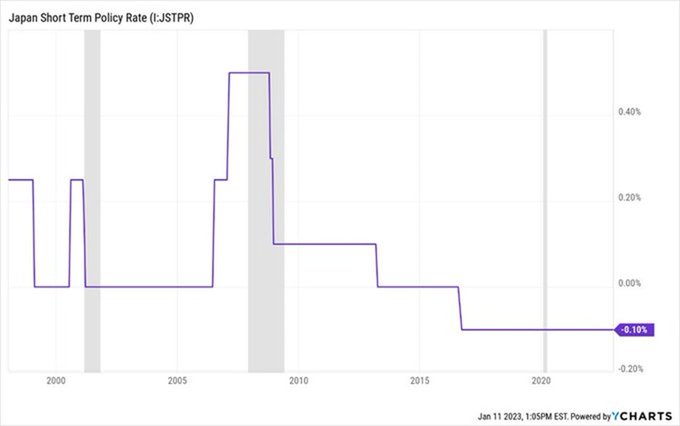

Japan has had negative interest rates for 6 years and has been struggling for more than 20 years with disinflation. This changed with COVID, which catapulted inflation to 4% today, the highest rate in the last 30 years!

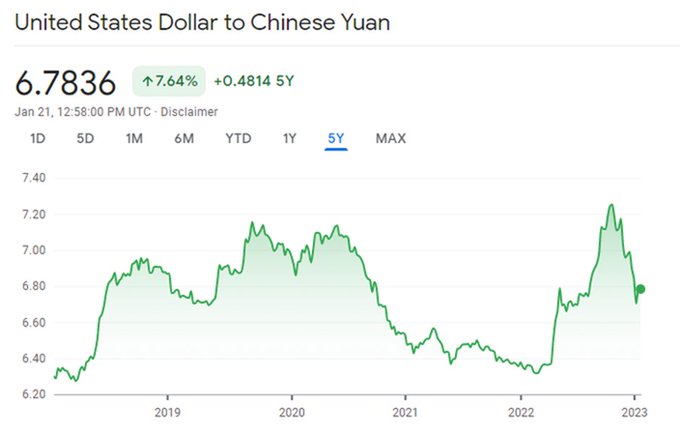

If China wants to remain the “low cost factory” of the world, it cannot afford inflation higher than 2%. They also cannot afford a strong Yuan.

Despite the fact that inflation is at its highest since the 80s, the central bank of Japan (BoJ) maintains a negative interest rate of -0.10% but widened in December 2022 the band around the bond yield target of +/ -0.25bps to +/- 0.50bps.

The expectation is that rates in Japan will increase no later than 2024 when Haruhiko Kuroda, the current BoJ president, retires.

3. CORPORATE PROFITS

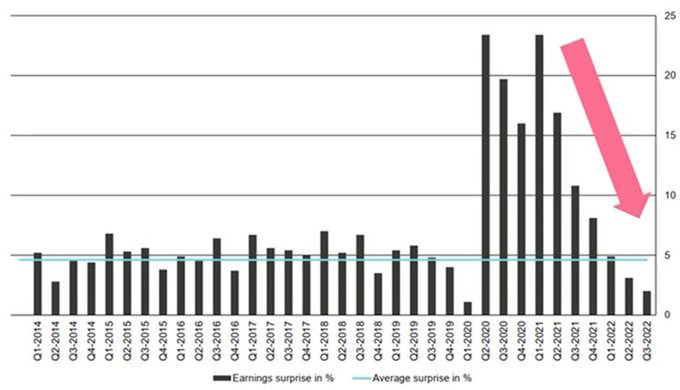

S&P 500 corporate earnings have been surprising with a sequential slowdown

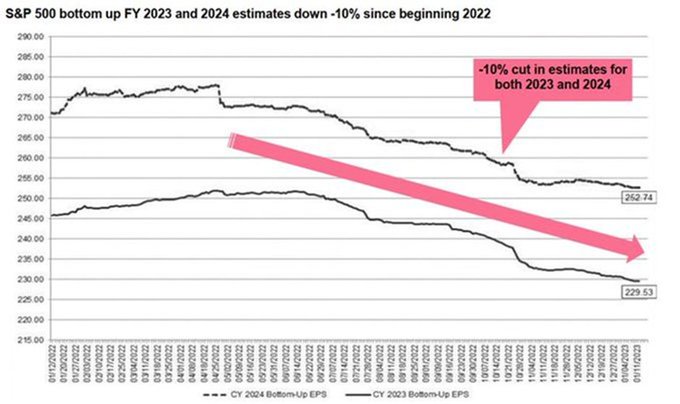

S&P 500 EPS Estimates for 2023 and 2024 are down -10%

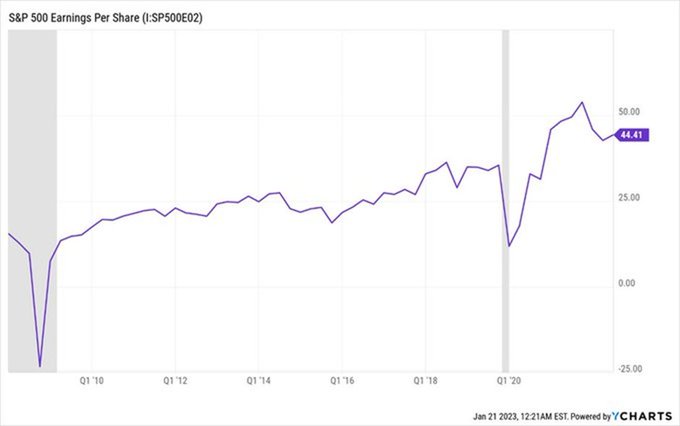

Even though earnings are down, they have remained pretty solid, being down only 3.50% in the last 12 months.

4. REAL ESTATE

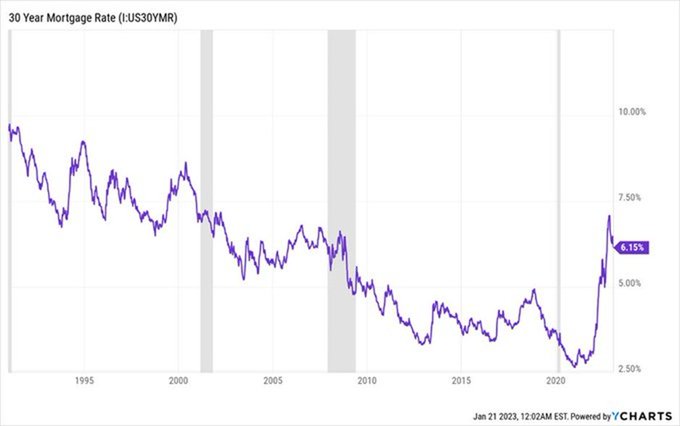

The 30-year mortgage rate rose to 6.95% in November, its peak in the last 20 years but has since dropped to 6.15% today.

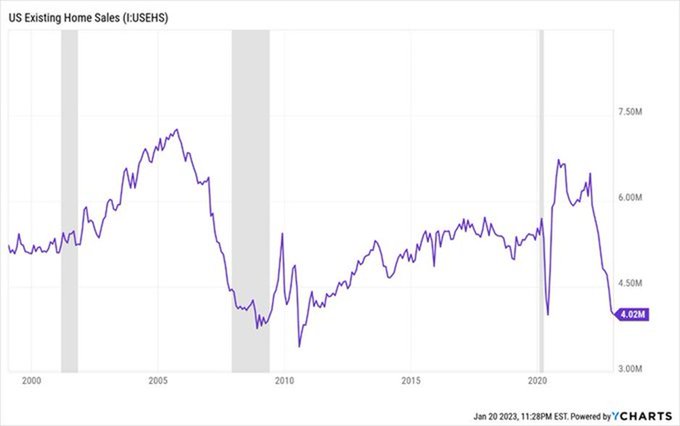

Existing home sales have plummeted to levels not seen in the last 30 years.

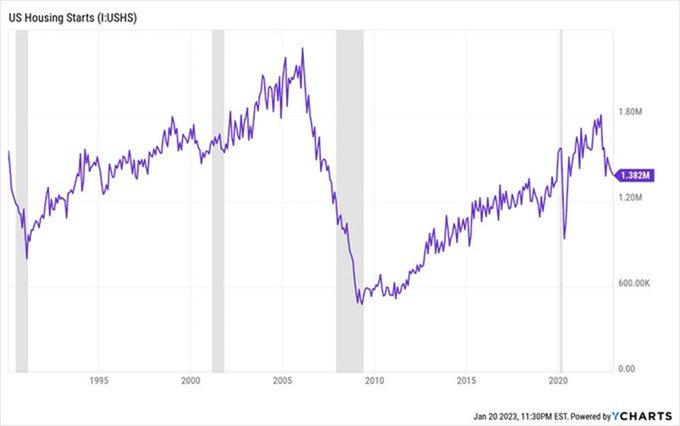

New home construction has fallen 17% in the last 12 months with a downward trend.

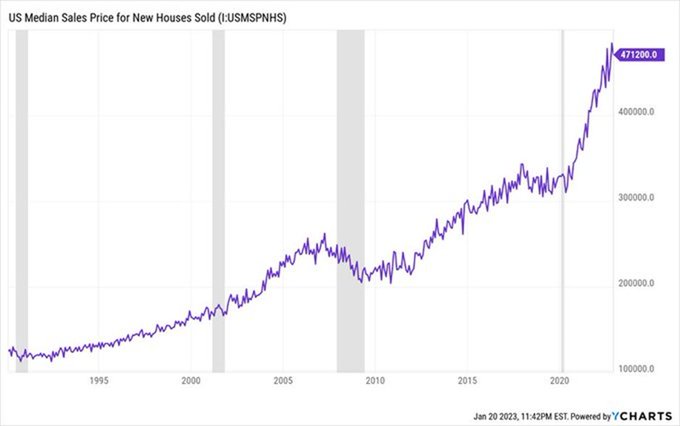

Despite everything, the average price of a new home is USD 471,200, an all-time record level. The question is, for how long?

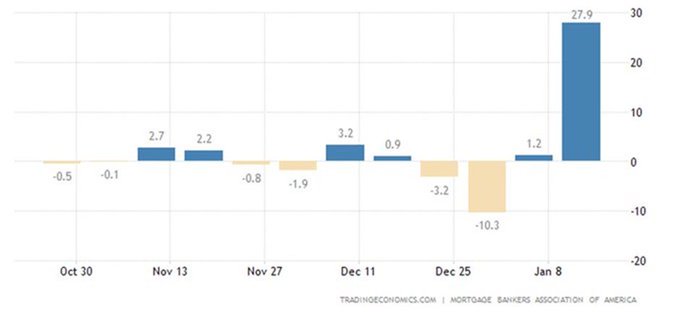

In January the demand for mortgages shot up 28% as mortgage rates fell from 6.48% to 6.33%, indicating that the desire for a home remains strong.

5. THE CONSUMER

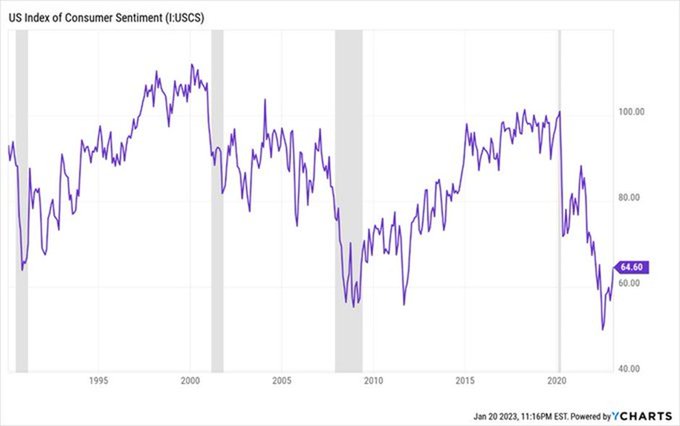

Higher interest rates, a potential recession and high prices made consumers less confident in the current state of the economy. However, the consumer sentiment has been recovering since July 2022.

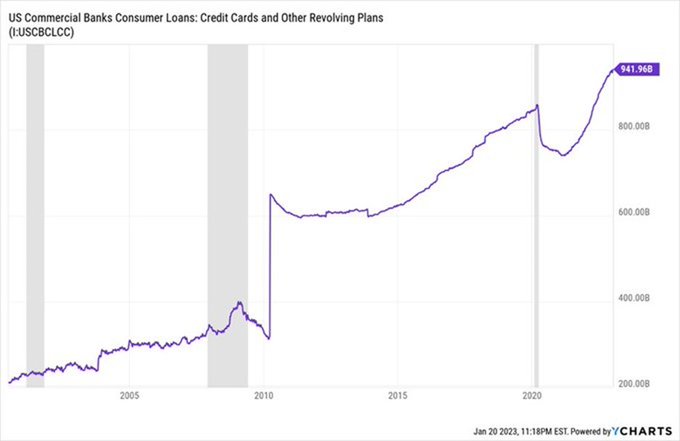

Credit card debt is near its all-time high. With higher interest rates, it will be an increasingly difficult burden for the American consumer to bear.

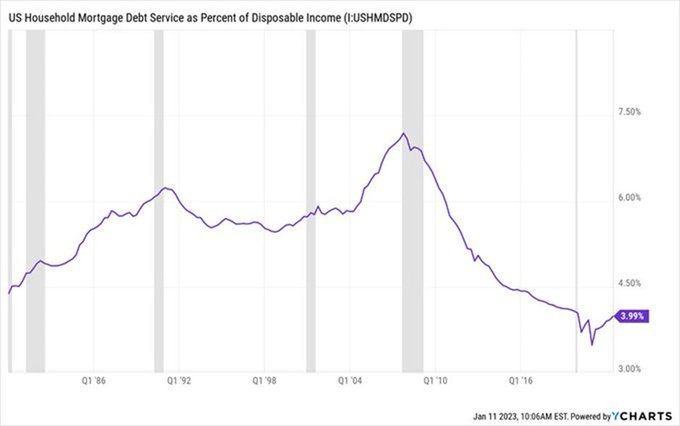

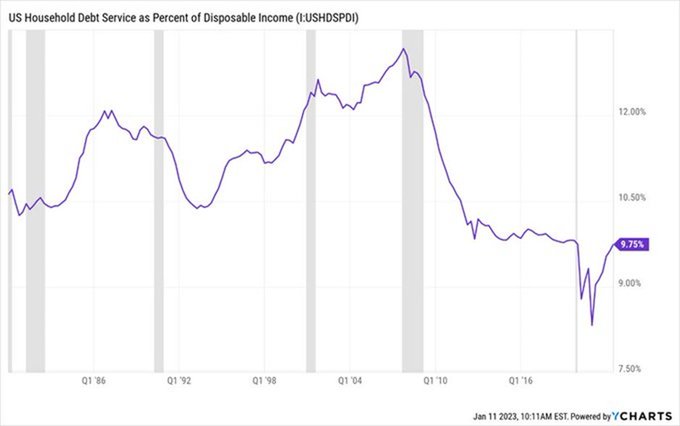

Despite rising mortgage rates, household mortgage debt service as a % of disposable income remains low. Most Americans have been able to (re-)finance their long term mortgage at low rates so the current rise hasn’t hit them (yet).

Total US household debt service as a % of disposable income is at a historically low level, indicating that the American consumers have managed to keep their finances under control.

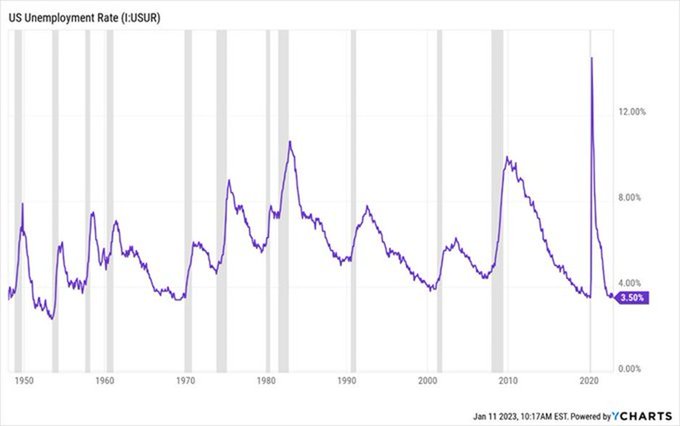

Unemployment reate is at 3.50% -> it’s a record low. This indicates that the real economy (mainstreet) remains robust.

6. STOCK MARKET

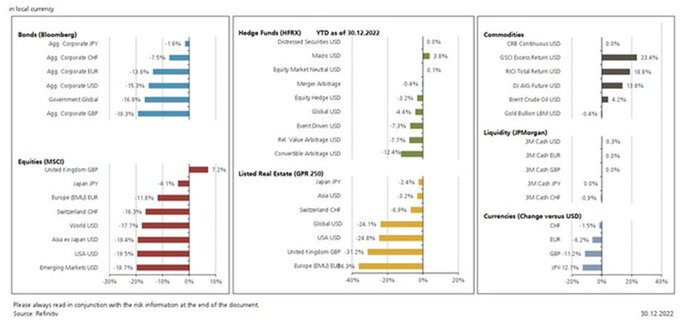

Several markets corrected sharply, including some typical safe haven assets like bonds, gold and the Swiss Franc that usually hedge against corrections.

7. CONCLUSION

It seems that the consumer emerged stronger from COVID-19 and has enough reserves to face the current high rates. Real estate hasn’t gone down in price yet, probably because most Americans managed to refinance their mortgages at very low long-term rates, so the short-term increase hasn’t affected them (yet). The markets have already corrected strongly including equities and fixed income. The market may have bottomed out in October 2022, but we have to see how the market, specially the real estate market, reacts if rates continue to rise globally. This can take a few months to play out.