Let’s start with the basics: What are TIPS?

TIPS stands for Treasury Inflation-Protected Securities.

TIPS are a type of Treasury security whose principal value is indexed to inflation. When inflation (CPI) rises, the TIPS’ principal value is adjusted up. If there’s deflation, the principal value is adjusted lower. Like all Treasuries, TIPS are backed by the U.S. government.

The coupon payments are based on a % of the adjusted principal, so you can benefit from higher income payments when inflation is rising as well. At maturity, you receive either the adjusted higher principal or the original principal value.

At maturity, a TIPS investor would receive either the adjusted higher principal or the original principal value. In other words, TIPS never pay back less than the initial principal value at maturity.

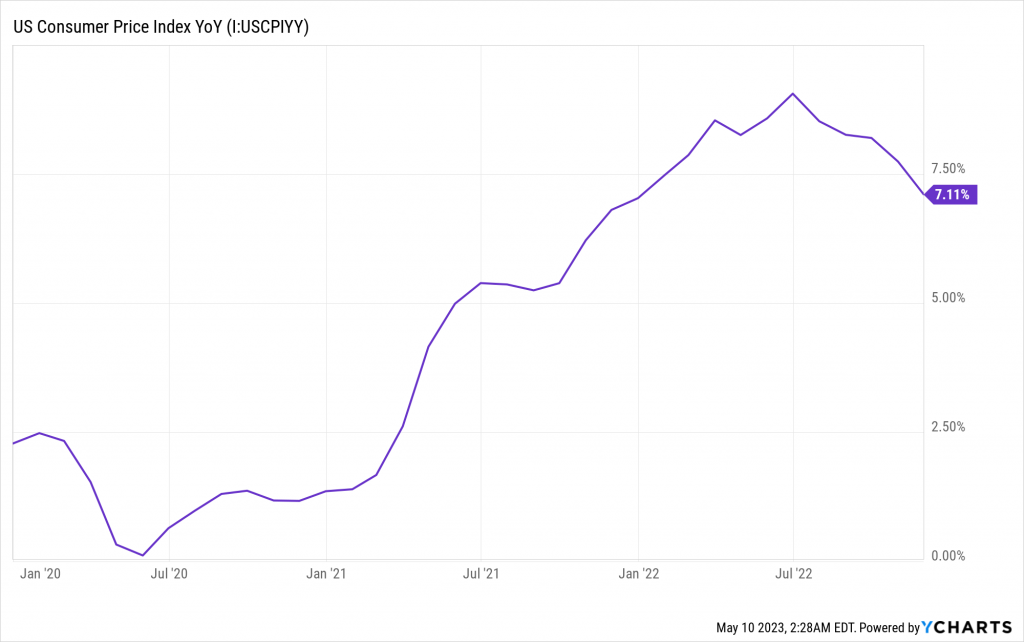

If TIPS protect against inflation, and inflation is at its highest point since the 70’s, why are TIPS down this year (2022)?

It’s not “normal” for TIPS to fall so much, but it’s common for TIPS returns and the rate of inflation to diverge over short periods of time. TIPS prices have fallen more than the principal has adjusted higher, resulting in negative total returns. TIPS can help protect investors against inflation over the long term, but they aren’t a hedge against inflation in the short run, because price changes may more than offset the principal adjustment over shorter periods of time.

Don’t forget, TIPS are still bonds, meaning their prices and yields move in opposite directions. Like most fixed income investments this year, TIPS yields have surged, pulling their prices lower.

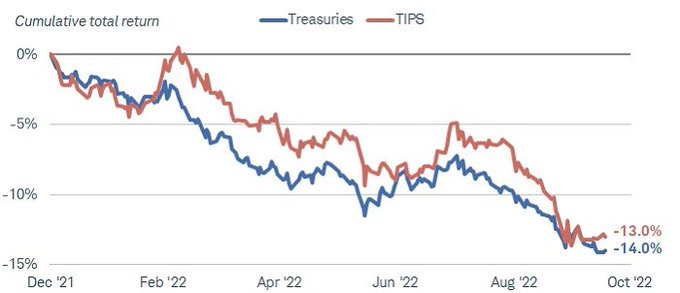

The Bloomberg U.S. TIPS Index is down 13% this year, while the Bloomberg U.S. Treasury Index is down a bit more, with a negative 14% total return over the same period. So even though the CPI is up 8.2%, the price decline more than offset that positive principal adjustment.

What drives the prices of TIPS?

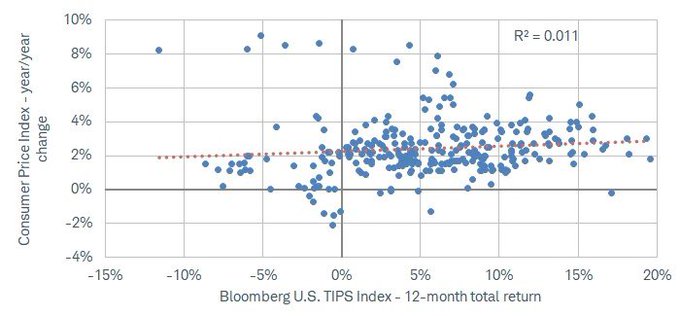

Most people don’t know this, but historically and surprisingly, there hasn’t been much of a relationship between the total return of the TIPS index and the change in inflation rate.

The chart below compares the year-over-year change in the CPI to the 12-month rolling return of the Bloomberg U.S. TIPS Index since index’s inception in 1997. Although the trendline is upward sloping, there’s not much of a relationship between the two measures.

That’s one more reason why TIPS can help protect against inflation over the long run, but why they shouldn’t be considered an inflation hedge in the short run.

Which environment is positive for TIPS?

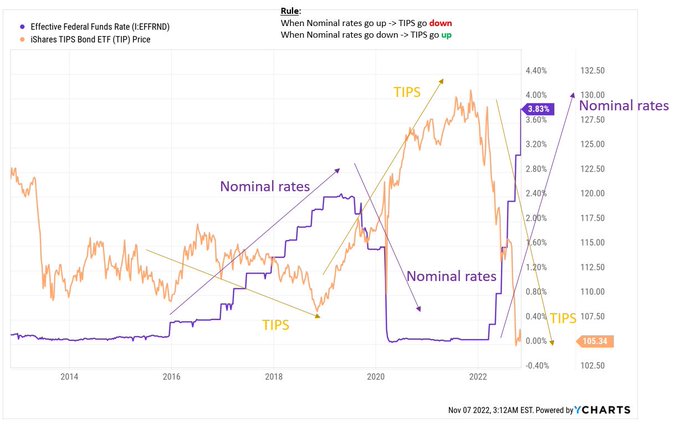

TIPS prices go up when: -> Nominal interests go DOWN OR -> Breakeven Inflation < CPI when nominal interest rates don‘t move Let’s look at each one separately.

When Nominal interest rates go DOWN -> TIPS prices go up. We can see on the below graph that Fed fund rates (nominal rates) and TIPs prices have a negative correlation.

When Breakeven Inflation (BEI) < CPI -> then TIPS prices go up (as long as nominal rates don‘t move)

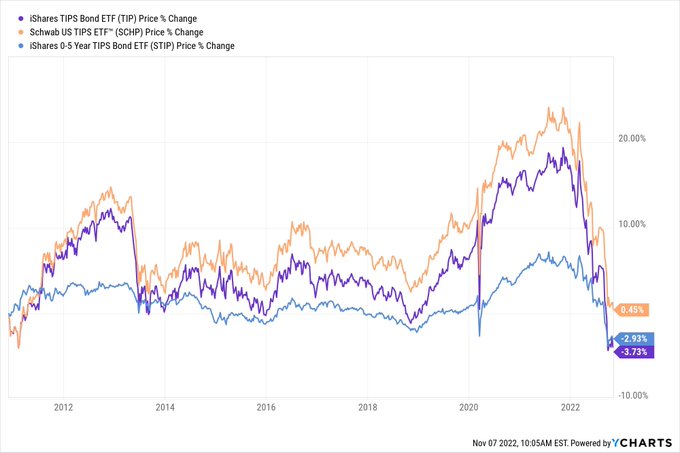

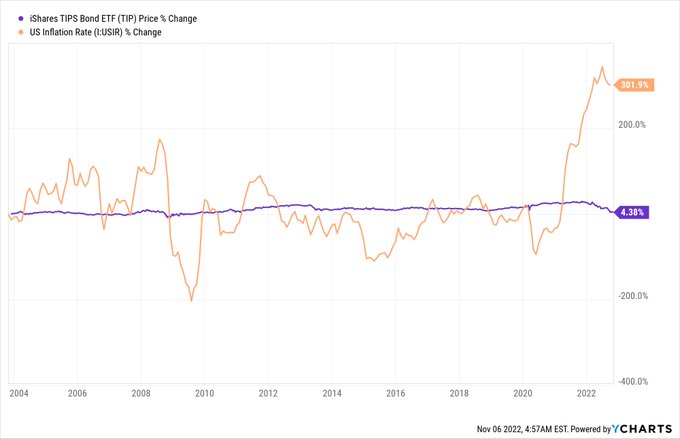

As we can see, TIPS are not as simple as a „protection against inflation“. This year TIPS have proven to be the wrong hedge. TIPS ETFs react similar to Treasury ETFs to interest rates moves (see graph below).

If we look at the long term returns, TIPS ETFs haven‘t offered an attractive return nor have they really protected against inflation.